6 min read

HK Web3 Festival 2023: When Asia's Crypto Pole Shifted

In April 2023, the Hong Kong Convention and Exhibition Centre played host to four days that felt less like a festival and more like a public service announcement. Hong Kong Web3 Festival pulled in over 10,000 attendees, 300 speakers, and around 100 Web3 projects across April 12–15. The numbers mattered, but the staging mattered more. Hong Kong was telling the industry that the regional centre of gravity for crypto was moving north.

Hong Kong opens

The opening session was political, not technical. Financial Secretary Paul Chan Mo-po delivered the keynote in person. HKMA's Clara Chan and Cyberport's Peter Yan King-shun spoke alongside HashKey's Xiao Feng. Changpeng Zhao headlined the afternoon fireside.

The political backdrop did the heavy lifting. In October 2022, Hong Kong had published its policy statement on virtual assets, signalling that the city wanted to host crypto activity again after years of attrition. By April 2023, the SFC's consultation on a licensed Virtual Asset Trading Platform regime was in its closing weeks. The conclusions landed on 23 May 2023, and the regime took effect on 1 June, including the headline detail that licensed platforms could serve retail investors under defined guardrails. The festival was the political theatre announcing what was about to be law.

Singapore tightens

The contrast was hard to miss. Singapore had spent the previous twelve months walking the other direction. In January 2022, MAS banned crypto firms from advertising in public spaces and through influencers. That August, MAS Managing Director Ravi Menon called crypto "highly hazardous" for retail investors and reframed the regulator's stance as "Yes to digital asset innovation, no to cryptocurrency speculation." In October, MAS opened a consultation on retail safeguards, proposing to bar credit card payments for crypto, ban trading incentives, and prohibit retail margin and lending.

The backdrop made the shift inevitable. Three Arrows Capital, Singapore-based, had collapsed in June 2022. Terraform Labs's UST implosion a month earlier had wiped out tens of billions in market value. And Temasek had written down its $275 million stake in FTX by November. Singapore's regulator wasn't moving against crypto in principle. It was moving against retail exposure to it.

What we kept hearing on the floor

Three threads dominated the conversations we had across the four days.

The first was jurisdiction. Operators wanted concrete answers about Hong Kong domicile timing. When would licences actually be issued? What did the wholly-owned-subsidiary custody requirement mean for existing wallet stacks? How long was the application queue going to be?

The second was institutional money. Family offices, brokerages, and a notable number of mainland-linked capital allocators were on the floor in a way that wasn't true at most crypto events. The conversations weren't about retail tokens. They were about access — how a regulated firm in HK could touch the asset class without taking compliance risk.

The third was infrastructure. Asian exchange operators wanted to know if their existing custody and wallet architecture would survive an HK licence application, or whether they would need to rebuild. The answers were uncomfortable for some.

The reality is messier than the contrast

The HK-versus-Singapore framing flattens what was actually happening. Hong Kong's regime is conservative on the rails. Custody must sit with a wholly-owned subsidiary, third-party custodians are not permitted, capital requirements are high, and the token universe approved for retail is narrow. Singapore is tighter on retail trading but materially more mature on the institutional layer, with deeper banking rails, more established custody providers, and a longer track record under the Payment Services Act.

Most operators we spoke to were not picking one. They were hedging. Entities in both jurisdictions, retail-facing licences in HK, institutional and treasury operations in Singapore, and contingency planning for a third base in Dubai or Tokyo. The smart play in April 2023 was not betting on a winner. It was building optionality.

What this means for the infrastructure layer

New jurisdictions create new entrants. New entrants make the same choices about custody, wallet operations, key management, and compliance evidencing. The Hong Kong wave was visible at the festival: exchanges, brokerages, and payment platforms preparing to apply for VATP licences or sub-licence under existing operators. None of them wanted to spend the next twelve months building wallet infrastructure from scratch when listings, liquidity, and compliance work was the actual job.

What we took back

April 2023 was the moment when "Asia's crypto centre of gravity is shifting" stopped being a talking point and became something you could see in person. Hong Kong wasn't replacing Singapore. It was creating a second pole, and forcing every operator in the region to make a deliberate choice about where to put which entity. The festival was the announcement. The licensing regime that followed was the substance.

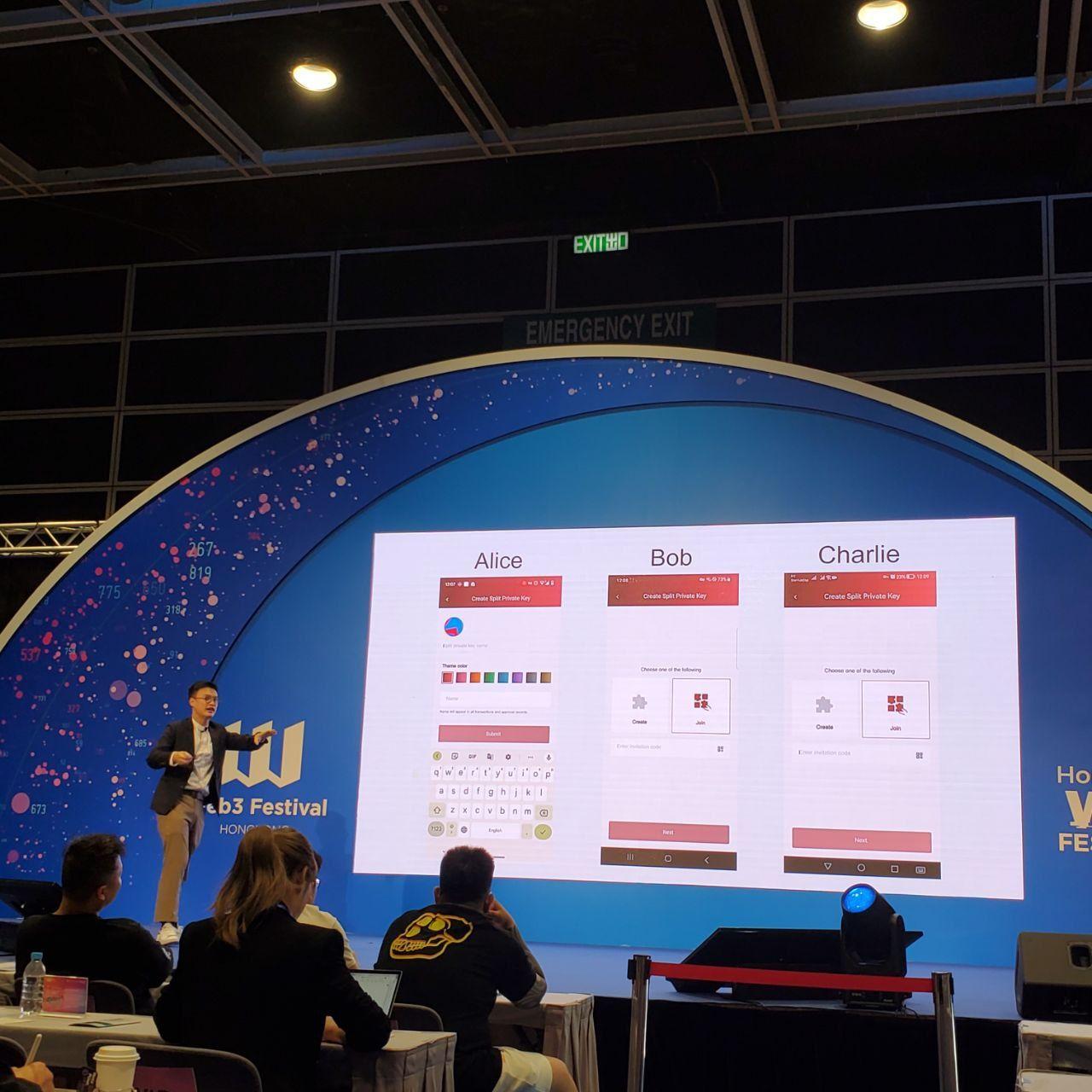

We're here!

Giving a speech isn't easy

but did it anyway!